Parent PLUS Loans Are a Double-Edged Sword for Black Borrowers

Approximately 43 million Americans collectively owe $1.5 trillion in federal student loan debt, but students aren’t the only ones drowning in student debt. Increasingly, parents, particularly Black parents, are taking out Parent PLUS loans and putting off retirement to help their children pay for college. Direct PLUS (Parent Loans for Undergraduate Students) loans, also known as “Parent PLUS” loans, account for $104 billion in outstanding federal student debt.

Parent PLUS loans are fixed-interest federal loans that parents of dependent undergraduate students can take out to help their kids cover the cost of college. These loans have less generous terms than student loans and lack many of the consumer protections that come with federal student loans. There are also a few important differences between federal student loans and Parent PLUS loans. The latter require a credit check, have higher interest rates, and less generous repayment terms than student loans.

Parent PLUS loans were originally intended for high-income parents who couldn’t cover their child’s account balance in one lump-sum payment. But as college costs have increased and financial aid has failed to keep pace with rising costs, more low-income parents and parents of color are relying on Parent PLUS loans to help pay for their children’s education. PLUS borrowing by Black parents is especially concerning because Black parents are borrowing outsized amounts relative to their incomes and assets and struggling with repayment, especially in retirement.

This brief is the fourth brief in a series based on qualitative data from the National Black Student Debt Study. It highlights the struggles of Black parents who assume Parent PLUS loans on behalf of their children and builds on “Jim Crow Debt: How Black Borrowers Experience Student Loans,” a report published by The Education Trust in partnership with Jalil B. Mustaffa, Ph.D., co-founder of the Equity Research Cooperative, and Jonathan C. W. Davis, Ph.D., director of research at the Equity Research Collaborative, which examines the crisis of Black student debt and the experiences of Black borrowers. The first three briefs examined “How Black Women Experience Student Debt,” the ways that “Student Debt Is Harming the Mental Health of Black Borrowers,” and how “Income-Driven Repayment Plans Fail Black Borrowers.”

In recognition of the needs of Black borrowers, The Education Trust is encouraging Congress and the Biden administration to address the root cause of the student debt crisis by making college more affordable by doubling the Pell Grant and creating a federal-state partnership to make public two- and four-year colleges debt free. We are also urging the Biden administration to cancel at least $50,000 in federal education debt and make Parent PLUS loans eligible for the proposed new income-driven repayment plan.

Parent PLUS Loans Were Originally Meant for High-Income Parents, But High College Costs and Insufficient Financial Aid Are Pushing Black Parents to Borrow

Parent PLUS loans are federal education loans taken out by parents (be they biological, legally adoptive, or in some cases, a stepparent) of dependent undergraduate students attending college at least half time. These loans are held solely by the parent. Parent PLUS loans can be used to pay for tuition, fees, and other education expenses up to the cost of attendance, less any scholarship and grants a student has received. In 2016, Parent PLUS loans accounted for 23% of all federal education loans disbursed for undergraduates.

When Parent PLUS loans were first introduced in 1980, annual borrowing was capped at $3,000, or $10,000 in today’s dollars. In 1992, borrowing caps were eliminated, and parents were allowed to borrow up to the cost of attendance, less any scholarships and grants, if they passed a credit history check. Initially, PLUS loans were intended for high-income and high-asset parents who needed liquidity and could not pay for their child’s education upfront. Increasingly, though, more parents with low incomes and low wealth are turning to PLUS loans because the scholarship, grant, and loan aid available to their children is insufficient to cover college costs, which have risen dramatically as state funding for public colleges has declined. A college education is increasingly unaffordable for most Americans — but especially for Black Americans. Because of the racial wage and wealth gaps, Black families have fewer financial resources to draw on to pay for college.

Financial aid rarely covers the full cost of college — which includes tuition and fees, room and board, transportation, books and supplies, and other expenses — even for the lowest-income students, who, theoretically, should not be expected to pay anything for college. Across all institution types, there is a gap between the average total cost and the average awarded aid for students. In the 2020-21 academic year, the full costs of college for first-year, full-time undergraduate students at public two-year, public four-year, private four-year, and for-profit colleges were $15,900, $25,700, $54,500, and $33,500 respectively. The widest gaps in cost and aid were at nonpublic institutions: $13,300 at private colleges and $10,100 at for-profit colleges. Public four-year and two-year colleges had gaps of $2,700 and $1,700 respectively. The largest source of aid offered by every institution type, except private colleges, was student loans, which ranged from an average of $4,800 at public two-year colleges to $8,700 at private colleges (see Figure 1).

Black Families Have Fewer Resources to Pay for College

Black families rely heavily on federal financial aid because they have fewer financial resources due to structural racism. The racial wage gap creates the conditions that force Black students to borrow more than their peers and Black parents, who have lower incomes than their White counterparts, to take out PLUS loans. In 2021, the median income for Black families was $58,728 compared to $94,447 for White families. But that’s only part of the story.

The racial wealth gap — which reflects the accumulated negative effects of centuries of systemic racism, including but not limited to slavery, Jim Crow laws, redlining, lending discrimination, and labor market and wage discrimination — makes things worse. In 2019, the median Black household had just $24,100 in wealth next to $188,200 for the median White household. What’s more, obtaining a higher education does not erase that gap. In fact, the median Black household headed by a person with a bachelor’s degree has less wealth than the median White household headed by a person without a high school diploma. According to a 2021 report by Andre Perry, Ph.D., a senior fellow at Brookings Metro and a scholar-in-residence at American University, 52% of Black households with student loans have zero or negative wealth, versus just 25% of Black households without student debt.

Noelle, who intentionally avoids looking at how much she owes, notes that generational wealth gave some of her peers a leg up:

“I feel like systemic racism is so real … There are a lot of people who do not have … loans because their parents have generational wealth that has allowed them to [help] their children to go forward and get this leg up. So, while I don’t feel that any parent is obligated to get their child started at a certain space, I am very aware that I have a number of peers who have no debt. That’s not something my mom ever complained about having or taking out for us, but I think it’s overall just the system that exists [and] that sucks.”

Additionally, Black parents of dependent students have the lowest annual incomes of any racial or ethnic group and highest financial need as determined by FAFSA (see Figure 2). The FAFSA formula used to determine financial need uses income, certain assets, family size, and other factors to calculate an Expected Family Contribution (EFC). A zero EFC indicates the greatest financial need. However, having an EFC of zero does not mean that a student’s full cost of attendance will be covered by financial aid. Students with a zero EFC are eligible for the maximum Pell Grant award of $7,395 for the 2023-24 academic year. Black students have the lowest average EFCs, and the rate of students with a zero EFC is highest among Black students.

Parents whose children have borrowed the maximum annual loan amount are more likely to take out a Parent PLUS loan. The financial aid system is yet another factor that makes it needlessly hard for Black students to attend college without they or their families sinking deeply into debt.

The Minimal Credit Check for Parent PLUS Loans is A Double-Edged Sword

Unlike student loan borrowers, Parent PLUS loan applicants must pass a credit check. To be approved, the parent must not have an “adverse credit” history. An applicant’s credit history may be considered adverse if within the five years preceding the date of the credit check, they have:

- an account in default, a bankruptcy, repossession, foreclosure, charge-off/write-off of federal student aid debt, wage garnishment, or tax lien;

- an overdue balance greater than $2,085 that is more the 90 days delinquent as of the date of the credit check or has been placed in collections or charged off in the prior two years.

If denied, a student can use a credit-worthy endorser, or if there are inaccuracies in the report, they can provide documentation to prove that their parent should have been approved. If a parent’s application is denied, a student will be offered an additional unsubsidized direct loan of $4,000 per year for their first and second years and up to $5,000 per year for their third year and beyond. However, this may not be enough to make up for the shortfall.

Income and assets are not considerations in determining eligibility for a Parent PLUS loan, so low-income and low-wealth parents can qualify for loans that they may struggle to repay. Unfortunately, many low-income families have few other options to cover high college costs, especially at four-year colleges. Many of our study participants noted that Parent PLUS loans were a last resort, and that college would have been out of reach for them or for their children without access to these loans.

Marissa notes that, as a student from a low-income background, a Parent PLUS loan was what allowed her to attend Howard University:

“The Pell at that time was not a lot. And our EFC at that point was zero. But even though it was zero, it still did not help with paying for Howard. Because Howard is a private university. So, my dad took out a Parent PLUS Loan. So that’s how I was able to do that.”

Parent PLUS Loan Repayment Terms Make It Harder for Black Parents to Repay

Black borrowers in the study highlighted the multigenerational toll of Parent PLUS loans. Many parents said they were unable to afford their monthly payment currently or had struggled to afford it at some time in the past. This caused many to rely on forbearance or deferment, which pauses payments while interest still accrues. Even parents who were able to make their monthly payment found repayment stressful. Most were frustrated that such a large portion of their income goes to repayment. Many feel that repayment is dictating their life choices in a negative way. This is not surprising. Black borrowers tend to struggle most with federal education loan repayment. But Parent PLUS loan repayment can be particularly challenging for Black borrowers, thanks to high interest rates, the shorter repayment timeline before retirement age, and a lack of direct access to income-driven repayment plans, which base a borrower’s monthly payment on their income and household size.

Parent PLUS loans have a higher interest rate than federal student loans. Parent PLUS loans disbursed in the 2022-23 academic year have a fixed 7.54% interest rate compared to 4.99% for undergraduate student loans. Low-income student borrowers can get subsidized loans, which don’t accrue interest until six months after a student graduates, leaves school, or drops below half time, but low-income parent borrowers cannot get this subsidy.

Parent borrowers are expected to begin repayment as soon as the loan is disbursed. In contrast, undergraduate student loans don’t require repayment until a student graduates, is enrolled less than half time, or leaves school. Student borrowers can also get a one-time, six-month grace period before repayment is required. Parent PLUS borrowers can ask to have their loan deferred until their child graduates, drops below half time, or leaves school. But interest will accrue while the loan is in deferment, and once the deferment ends, that accrued interest will be capitalized, causing the balance to increase.

Walter explained how multiple deferments affected his balance:

“Part of why the bill is so high now is because I deferred and deferred and deferred, because I couldn’t afford to start paying on it when I first started getting the loans. So, now I’m, fortunately, at a point where I can start paying on it.”

Also, having college debt undercuts a person’s ability to save for retirement, and that’s a serious concern for older Black parent borrowers, who have less time left to make retirement contributions and pay off debt. When asked if they had borrowed or taken money from retirement accounts, 22.1% of Black parent borrowers said they had done so compared to only 8.9% of White parent borrowers.

Better access to federal income-driven repayment plans has the potential to help financially strained borrowers and reduce default among Black parent borrowers. Income-driven repayment (IDR) bases a borrower’s monthly payment on 10% or 15% of their discretionary income and cancels the remaining balance after 20–25 years of qualifying payments. These plans aren’t perfect, and borrowers in our study said they felt like they had a lifetime-debt sentence because the design of existing programs often results in ballooning balances for many borrowers because their reduced monthly payment may not be enough to cover the interest that accrues monthly. That said, these plans can be an important financial lifeline, especially for the lowest income borrowers, whose payments can be a low as $0 a month.

Many study participants were concerned about parents struggling with Parent PLUS loans. Unfortunately, while many of them would like to help their parent(s) repay those loans, these Black borrowers are at a disadvantage because Black workers tend to have a lower return on investment for their degree(s) than White workers, due to discrimination in the labor market. In 2020, Black workers aged 25 to 64 who held a bachelor’s degree or higher and worked full time and year-round had median earnings of $65,135, compared to $77,162 for White workers with only a bachelor’s degree. In fact, Black workers need a professional degree to outearn White workers with a bachelor’s degree.

The growing use of Parent PLUS loans by Black parents and their struggles with repayment illustrate that higher education finance and financial aid policies have failed. It is not sustainable to saddle two generations with debt to pay for one degree.

Recommendations

So, what can we do? Student debt is growing, as is the number of Parent PLUS loans held by older Black borrowers. But while the situation is dire, it’s also a byproduct of failed and intentionally racist policies going back generations. Changing those policies and making college more affordable for Black borrowers are, therefore, keys to solving the student debt crisis and reducing the need for students and parents to borrow. The Education Trust recommends the following:

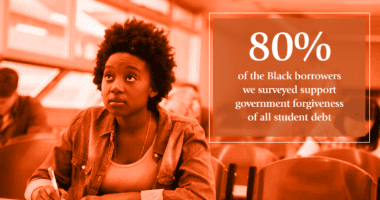

- More than 80% of the participants in the National Black Student Debt Study think the federal government should cancel all student debt, and policymakers would be wise to listen to them and help ease their debt burden. The Education Trust supports canceling at least $50,000 of federal student debt per borrower and opposes limiting eligibility for cancellation by income, loan type, or degree level (e.g., undergraduate versus graduate degree).

- Make Parent PLUS loan borrowers whose children received a Pell Grant eligible for up to $20,000 in loan cancellation.

- Current and future Parent PLUS borrowers should be eligible for all income-driven repayment (IDR) plans and Public Service Loan Forgiveness (PSLF) without having to consolidate.

- Interest rates for Parent PLUS loans should be reduced and set at the rate for undergraduate student borrowers.

- Access to Parent PLUS loans should not be restricted without more affordable financial aid options to replace them.

- The Biden administration should continue to make improvements to income-driven repayment (IDR) plans to make monthly payments more affordable, reduce negative amortization, and shorten the time-to-forgiveness window.

- To make college affordable, Congress should double the Pell Grant and create federal-state partnerships to make public college debt free.

Jim Crow Debt

by Jalil B. Mustaffa, Ph.D. and Jonathan DavisStudent debt has been a crisis for years, and the pandemic has only exacerbated matters for many borrowers. This is especially true for Black borrowers, who ar…

How Black Women Experience Student Debt

Forty-five million Americans collectively owe $1.7 trillion in student loan debt, and women hold nearly two-thirds of it. But because of the gender pay gap, wo…

How Student Debt Harms Black Borrowers’ Mental Health

by Ed TrustApproximately 45 million Americans carry $1.7 trillion in student loan debt, but the financial challenges facing Black borrowers are numerous. Black students a…

Income-Driven Repayment Plans Fail Black Borrowers

by Victoria Jackson and Jalil B. Mustaffa, Ph.D.Approximately 43 million Americans collectively owe $1.6 trillion in federal student loan debt, but this debt is not borne equally by all. Black borrowers are …

{kind=link}

{kind=link}

{kind=link}

{kind=link}